THE PULSE: CONSTRUCTION MATERIALS MARKET ANALYSIS

- The Federal Reserve has held rates steady for just over ten months now, at 5.3%. The most recent update indicates that the Fed will likely cut rates only once before the end of the year as they attempt to achieve a “soft landing.”

- The Federal Open Market Committee raised their 2024 outlook on inflation to 2.6%, or 2.8% when excluding food and energy. A return to 2% is not expected until 2026. The Consumer Price Index (CPI) was unchanged for the month and rose 3.3% over the last 12 months.

- The continuation of inflated housing prices, the presidential election, and whether or not we will truly see rate cuts are all things to watch in 2024 as they will have a significant impact on the overall economy

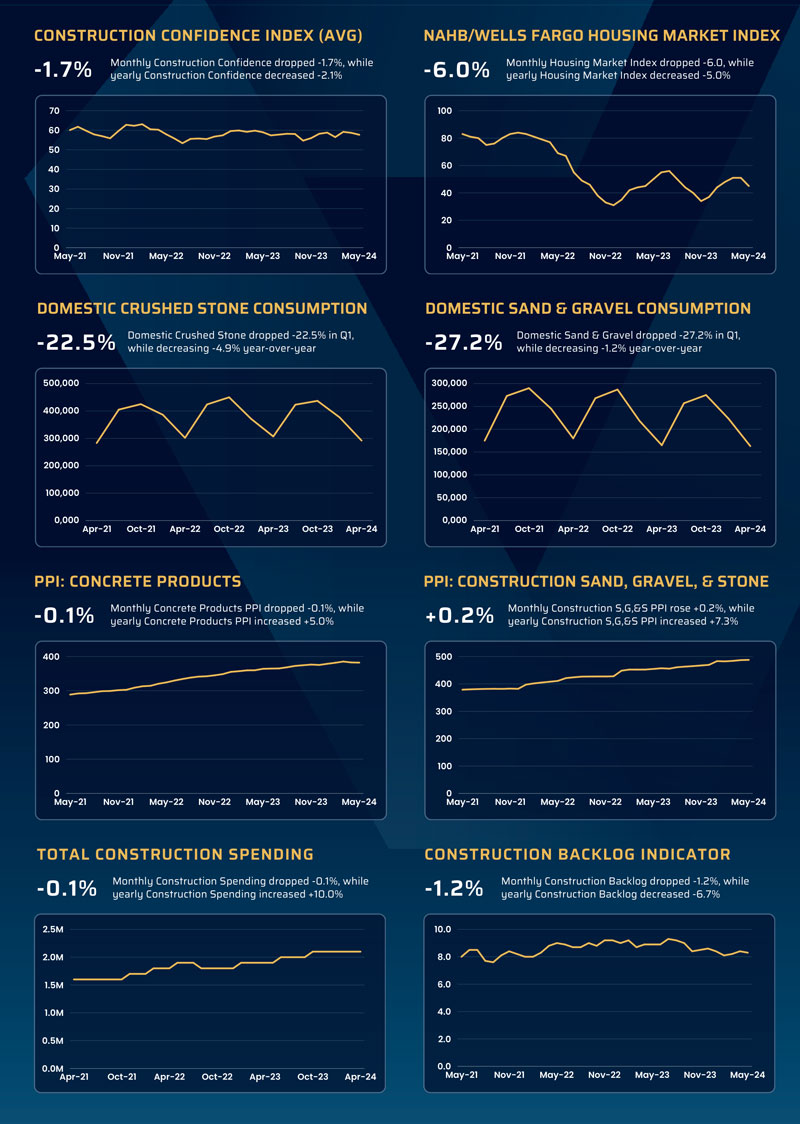

- Both Concrete Products and Construction Aggregates prices held steady this month, after consistent increases over the past year

- ABC’s Construction Backlog Indicator declined to a most recent monthly reading of 8.3 months in May 2024 from 8.4 months in April. This is down 0.6 months from May 2023, which was 8.9 months.

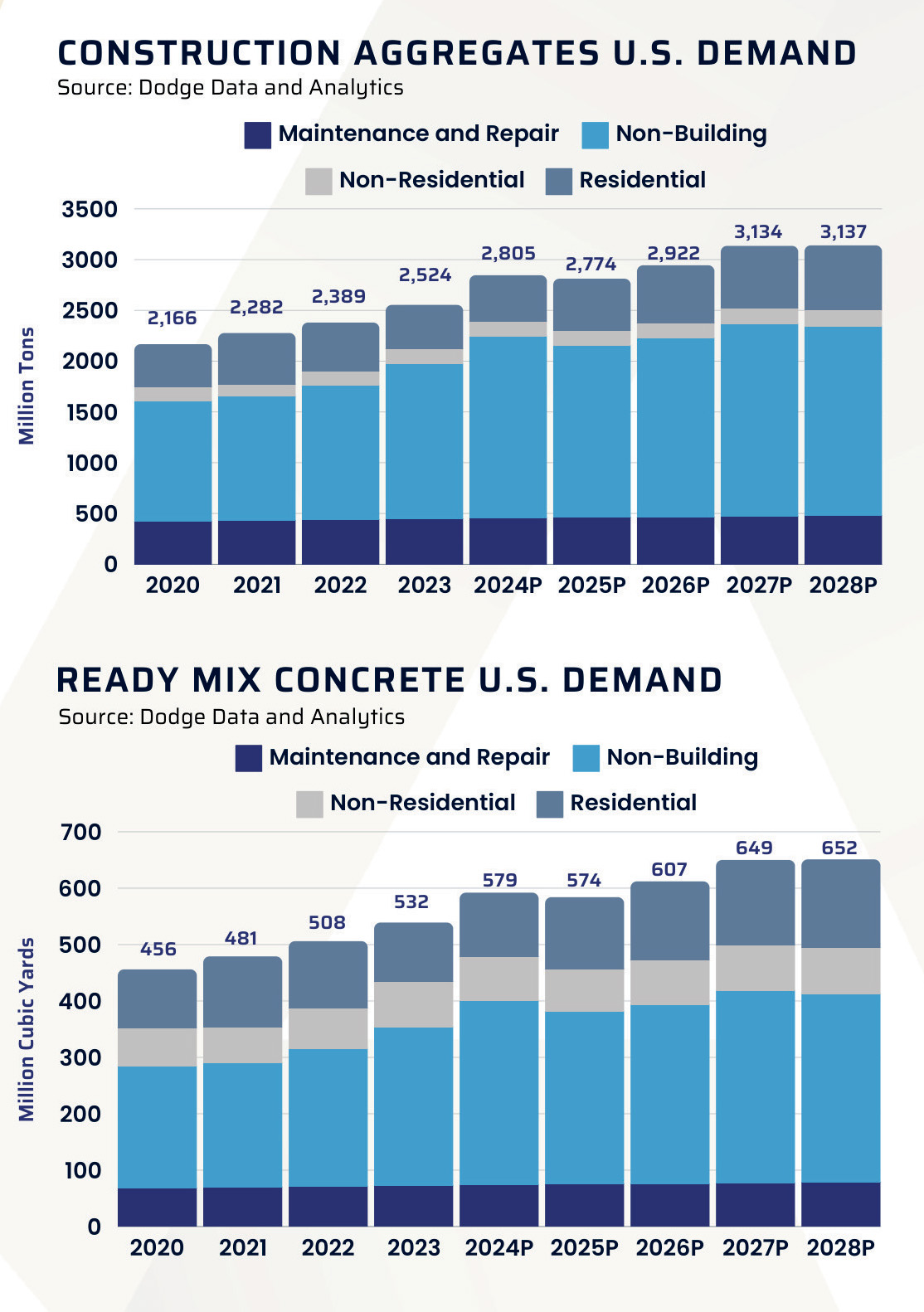

- The Infrastructure Investment and Jobs Act has provided a safety net to the Construction Materials Industry by increasing infrastructure investments which will help negate the possible slowing in residential construction due to higher interest rates and a slowing overall economy

PIERRE VILLERE’S MARKET ASSESSMENT

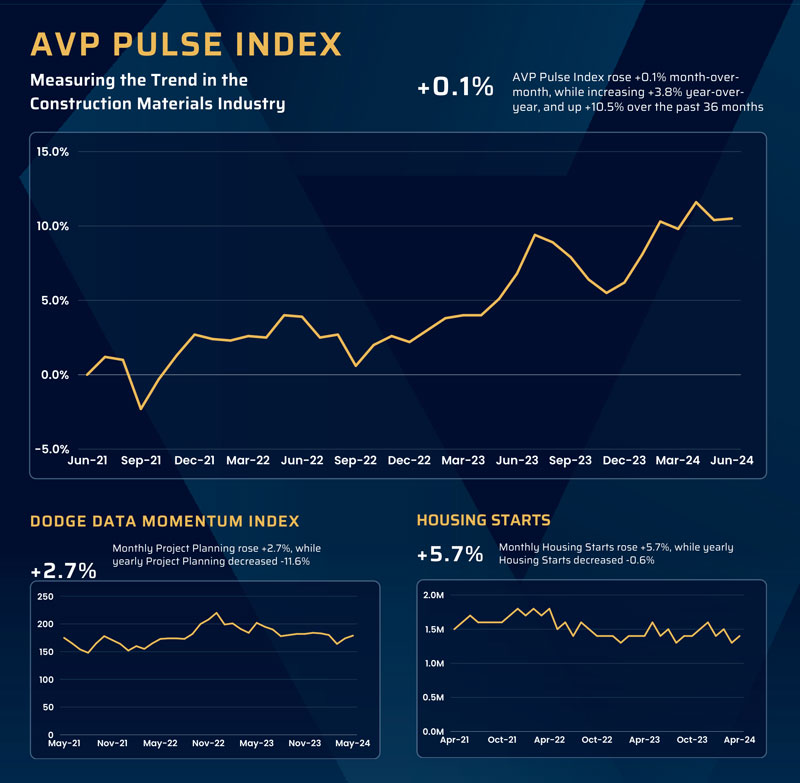

In the latest update on the construction materials industry, the AVP Pulse Index experienced a modest increase of 0.1% for the month, but continues to gain ground with steady, but not overly strong, year-over-year growth of 3.8%. Over the past 36 months, the index increased 10.5%, indicating a slight slowdown in growth within the sector compared to earlier this year. Industry stocks hit new all-time highs earlier this year, and there has been what we believe is a rotational pullback as profit-taking takes place, yet profitability remains steady, if not strong, at several of the major multi-nationals.

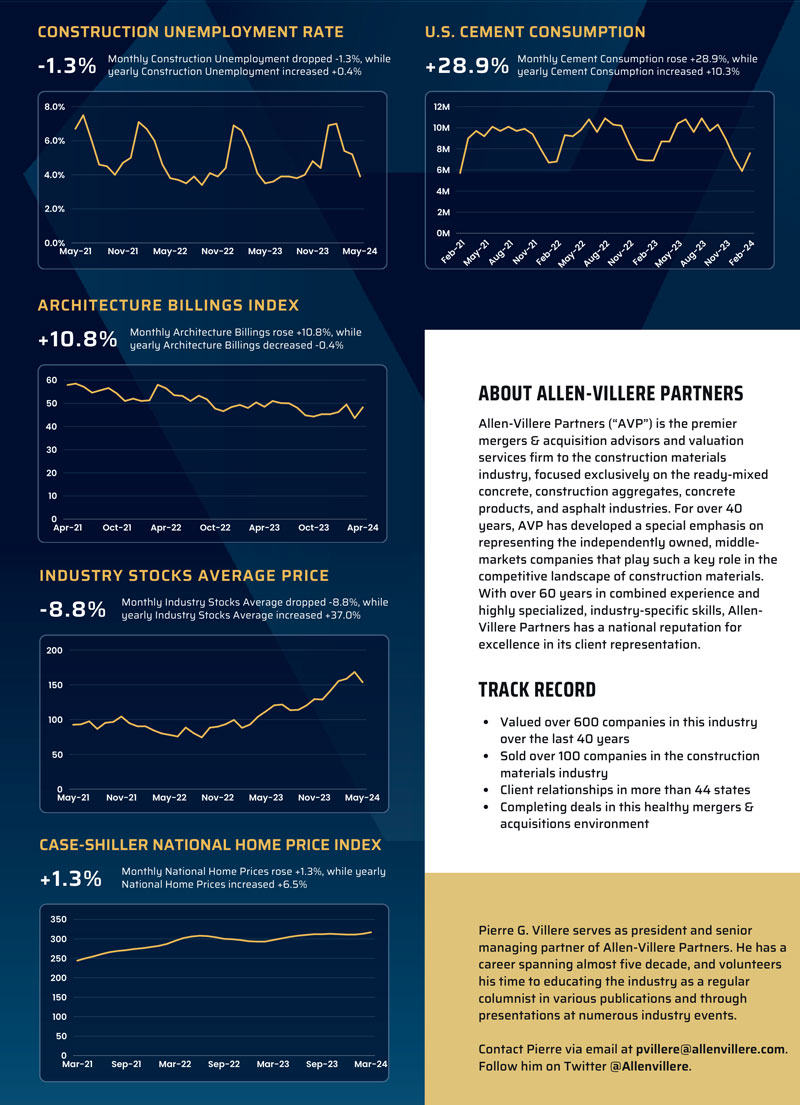

The first quarter saw big increases in cement consumption, with a 28.9% increase in monthly consumption, and 10.3% increase year-over-year, and further buoyed by a 5.7% increase in housing starts for the month. Amazingly, despite an adverse mortgage interest rate environment, year-over-year housing starts have held steady, down only a small -0.6%. Other strong showings in the Dodge Data Momentum Index and the Architectural Billings Index added strength to our algorithm and kept our Index in positive territory.

As has been the case for some time now, total construction spending remains steady if not robust, with only a marginal monthly pullback of -0.1%. Encouragingly, compared to the same period last year, total construction spending is up by a significant 10.0%.

In the view of Allen-Villere Partners, the construction materials industry is poised to remain healthy for the foreseeable future, buoyed by strong demand fueled by increasing federal outlays for construction projects under the Infrastructure Investment and Jobs Act (IIJA). the CHIPS Act, and the Inflation Reduction Act. Against this backdrop, coupled with the industry’s resilience and positive indicators such as pricing strength and sustained high construction spending, the outlook remains favorable. The industry’s ability to capitalize on these opportunities while navigating challenges underscores its enduring stability and potential for sustained prosperity. But clearly, and most significantly, while the Fed has preached “higher for longer” as a mantra for interest rates, they will start falling in the months ahead, although the timing is very uncertain. When they do start falling, we will see pent-up homebuyers, anxiously sitting on the sidelines, come flying off the benches. Likewise, commercial construction also hindered by high interest rates will surely experience a resurgence.

It is worth repeating that the AVP Pulse Index is a trend measure, like an arrow, albeit a crooked one; it points up or down depending on the direction of the construction industry. As stated above, the outlook is for continued growth and profitability for our industry based on the trailing trends and the overall positive direction of the Index over the past 36 months.