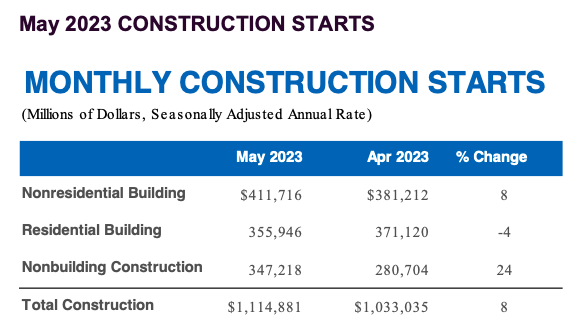

Total construction starts rose 8% in May to a seasonally adjusted annual rate of $1.11 trillion, according to Dodge Construction Network. Nonresidential starts rebounded following the decline in April, improving 8% thanks to a sizeable gain in manufacturing starts. During the month, nonbuilding starts improved by 24%, while residential lost 4%.

Highway and bridge starts gained 16%.

On a year-to-date basis through May, total construction starts were 6% below the first five months of 2022. Residential starts were down 25%, nonresidential starts were 1% lower, and nonbuilding starts gained 25%.

For the 12 months ending May 2023, total construction starts were 9% higher than the 12 months ending May 2022. Nonbuilding starts were 30% higher, while nonresidential building starts gained 26%. However, on a 12-month rolling basis, residential starts posted a 15% decline.

“May’s data is another sign that the construction sector is slowly splitting in two,” said Richard Branch, chief economist for Dodge Construction Network. “Public dollars are flooding into the manufacturing and infrastructure sectors, leading to significant growth over the last year. Meanwhile, the mostly private sectors of the building market like offices, multifamily and retail are struggling under the weight of higher interest rates, tightening lending standards and declining demand. The second half of the year is shaping up to be a challenging one. But, the insulation provided by manufacturing and infrastructure starts will stabilize the industry and lead to modest overall growth.”

Nonbuilding

Nonbuilding construction starts rose 24% in May to a seasonally adjusted annual rate of $347 billion. Utility/gas plants powered the increase as it jumped 53% over the month. Street and bridge starts moved 22% higher, and environmental public works increased 3%. Meanwhile, miscellaneous nonbuilding starts showed no change. Year-to-date through May, nonbuilding starts gained 25%. Utility/gas plants rose 76%, and miscellaneous nonbuilding starts were up 27%. Highway and bridge starts gained 16%, and environmental public works were up 11% on a year-to-date basis.

For the 12 months ending May 2023, total nonbuilding starts were 30% higher than the 12 months ending May 2022. Utility/gas plant starts rose 68%, and miscellaneous nonbuilding starts were 27% higher. Highway and bridge starts were up 22%, and environmental public works rose 18% on a 12-month rolling sum basis.

The largest nonbuilding projects to break ground in May were the $5.3 billion first train for the Port Arthur LNG project in Port Arthur, Texas, the $1.5 billion Southeast Connector Interchange highway project in Fort Worth, Texas, and the $925 million Amtrak/Metro Norwalk Bridge Replacement project in Norwalk, Conn.

Nonresidential

Nonresidential building starts rose 8% in May to a seasonally adjusted annual rate of $412 billion. The driving force behind the increase was manufacturing starts, which more than doubled in May. Commercial starts tumbled 20% in May due to a sharp pullback in office and retail starts, while hotel starts moved higher. Institutional starts fell just 1% in May with education starts falling, but healthcare increasing.

On a year-to-date basis through May, total nonresidential starts were 1% lower than that of 2022. Institutional starts gained 12%. Meanwhile, manufacturing starts were 11% lower, and commercial starts were down 7%.

For the 12 months ending May 2023, total nonresidential building starts were 26% higher than the 12 months ending May 2022. Manufacturing starts were 72% higher, institutional starts improved 22%, and commercial starts gained 12%.

The largest nonresidential building projects to break ground in May were the $1.9 billion Steel Dynamics aluminum plant in Columbus, Miss., the $1.9 billion Eli Lilly & Co facility in Indianapolis, Ind., and the $1.5 billion Ford Ohio EV plant in Sheffield, Ohio.

Residential

Residential building starts lost 4% in May to a seasonally adjusted annual rate of $356 billion. Single family starts retreated, falling 2% in May following four consecutive monthly gains. Multifamily starts shed 8%.

On a year-to-date basis through May 2023, total residential starts were down 25%. Single family starts were 31% lower, and multifamily starts were down 12%.

For the 12 months ending in May 2023, residential starts were 15% lower than that of 2022. Single family starts were 26% lower, while multifamily starts were up 9% on a rolling 12-month basis.

The largest multifamily structures to break ground in May were the $414 million North Cove mixed-use building in New York, the $190 million Albany Terrace and Irene McCoy Gains apartments in Chicago, and the $190 million The Kaye Luxury apartment tower in Seattle.

Regionally, total construction starts in May fell in the Northeast and West, while gaining in the Midwest, South Atlantic and South Central regions.