IN THIS UPDATED ANALYSIS PREPARED FOR ROCK PRODUCTS, HEADWATERS MB LOOKS AT SECOND-QUARTER 2016 AGGREGATES-INDUSTRY TRENDS SUCH AS MERGERS, STONE PRODUCTION AND PRICING.

By Brian Krehbiel

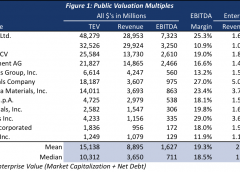

In Q2 2016, average valuation multiples for the publicly traded aggregates industry declined 2.3 percent and average EBITDA margins during the period increased from 18.9 percent to 19.3 percent compared to Q1 2016 (Figure 1, includes the constituents of Headwaters Aggregates Materials Index). Year over year, valuation multiples decreased by 8.4 percent while EBITDA margins widened to 19.3 percent from 17.2 percent. The publicly traded aggregates industry as a whole was trading at an average EBITDA multiple of 11.0x at the end of Q2 2016. However, the median multiple of 9.9x is the more relevant valuation metric for Q2 due to outlier multiples from Vulcan Materials and Martin Marietta of 18.7x and 16.2x respectively.

Source: FactSet

Aggregate Materials Index – Company Spotlight

International and domestic aggregates providers experienced growth in revenue and margins in Q2 2016.

Buzzi Unicem is an Italian cement and aggregate producer with operations in central Europe, Russia, Algeria, Mexico and the U.S. In the first six months of 2016, the company reported a 2.7 percent increase in cement sales and a 0.6 percent decline in ready-mix concrete versus the same period in 2015. In December, 2015, Buzzi Unicem increased its stake in Mexican cement and ready mixed concrete producer, Corporacion Moctezuma, SAB de CV and in 2016 the company has been investing heavily in a new kiln line at its cement plant in Maryneal, Texas.

Buzzi Unicem is an Italian cement and aggregate producer with operations in central Europe, Russia, Algeria, Mexico and the U.S. In the first six months of 2016, the company reported a 2.7 percent increase in cement sales and a 0.6 percent decline in ready-mix concrete versus the same period in 2015. In December, 2015, Buzzi Unicem increased its stake in Mexican cement and ready mixed concrete producer, Corporacion Moctezuma, SAB de CV and in 2016 the company has been investing heavily in a new kiln line at its cement plant in Maryneal, Texas.

Cemex S.A.B de C.V manufactures and distributes cement, ready-mix concrete and aggregates in more than 50 countries. Cemex recently reported modest Q2 2016 sales declines in all geographic divisions except for the U.S. and Mexico (which posted 3.0 and 7.0 percent increases respectively) for an overall 1.0 percent drop in sales versus Q2 2015. Cost reduction initiatives and lower energy costs allowed the company to reduce its cost of sales and ultimately still post a 6.0 percent increase in Operating EBITDA. In Q2 2016, Cemex divested of assets in Thailand and Bangladesh to Siam City Public Co Ltd for $53 million. Additionally, on May 2, 2016, Cemex announced an agreement to sell its cement plant in Odessa, Texas, two cement terminals and the building materials business in El Paso, Texas and Las Cruces, New Mexico to Grupo Cementos de Chihuahua for $306 million as part of its plan to sell as much as $1.5 billion in assets by the end of 2017.

Cemex S.A.B de C.V manufactures and distributes cement, ready-mix concrete and aggregates in more than 50 countries. Cemex recently reported modest Q2 2016 sales declines in all geographic divisions except for the U.S. and Mexico (which posted 3.0 and 7.0 percent increases respectively) for an overall 1.0 percent drop in sales versus Q2 2015. Cost reduction initiatives and lower energy costs allowed the company to reduce its cost of sales and ultimately still post a 6.0 percent increase in Operating EBITDA. In Q2 2016, Cemex divested of assets in Thailand and Bangladesh to Siam City Public Co Ltd for $53 million. Additionally, on May 2, 2016, Cemex announced an agreement to sell its cement plant in Odessa, Texas, two cement terminals and the building materials business in El Paso, Texas and Las Cruces, New Mexico to Grupo Cementos de Chihuahua for $306 million as part of its plan to sell as much as $1.5 billion in assets by the end of 2017.

Select Merger and Acquisition Activity

Acquisition activity continued in Q2 2016 as aggregate producers acquired mineral reserves and completed strategic acquisitions to increase vertical integration and geographic expansion (Figure 2). Summit Materials, and U.S. Concrete were active consolidators during the quarter.

Private Equity Transaction Activity and Valuations

GF Data Resources, a provider of detailed information on business transactions ranging in size from $10 million to $250 million, provides quarterly data from over 200 private equity firm contributors on the number of completed transactions. Figure 3 provides the number of completed transactions from GF Data contributors, the average EBITDA multiple and the average amount of debt utilized in the transaction computed as a multiple of EBITDA. The data, although not industry specific, does show valuations consistent with prior periods but the number of transactions were up from the prior quarter but still below the 67 transactions reported in Q4 2015.

Aggregates Performance

In 2016, publicly traded aggregates producers are outperforming the S&P 500 and the Dow Jones Industrial Average (DJIA) (Figure 4) with a 14.0 percent YTD return as of June 30, 2016. As seasonal construction picks up steam and construction activity as a whole continues to grow rapidly, the gap between aggregate producer returns and the general market have widened. This trend is expected to continue through 2016 given the current robust construction cycle underway. Vulcan Materials CEO Tom Hill pointed to two important factors in continuing this trend and delivering on projected results in Vulcan’s Q2 results press release: “(1) the ability of our customers to recover weather-delayed volume from the second quarter, which can be a challenge in a growing market, and (2) the absence of further delays in several large projects in key markets. And, as always, fourth quarter weather and the ultimate length of the construction season can impact our shipments in a given year.”

Construction Employment

One of the most prevalent topics in the construction industry is the current shortage of qualified construction labor. NBC News recently found that there are approximately 200,000 unfilled construction jobs in the U.S. as reported by the National Association of Homebuilders and that the Department of Labor reported that the ratio of construction job openings to hirings is at its highest level since 2007. The Associated General Contractors of America monthly construction employment report for June reiterated these findings. Construction employment increased in 39 states between June 2015 and June 2016, although half the states shed construction jobs between May and June 2016. This shedding of jobs despite strong demand for construction labor is evidence of the significant decline in the availablity of experienced construction labor.

Housing Starts

At the end of July 2016, seasonally adjusted annual housing starts were 1.21 million, up 5.6 percent in relation to the same period in 2015. June 2016 numbers showed 1.19 million annual starts. The general consensus is that 1.5 million new homes are necessary on an annual basis to keep up with population growth and the replacement of old homes, given current homeownership rates of 62.9 percent, the lowest level since the Census Bureau began tracking homeownership rates in 1965.3 Housing starts will need to grow an additional 24.0 percent to reach sustainable levels and growth will drive land development and infrastructure expansion benefiting the aggregate industry.

Construction Materials

Construction material prices rose 1.1 percent in June, but have fallen 2.5 percent year-over-year, according to an Associated Builders and Contractors analysis of Bureau of Labor Statistics data. As has been the story in recent months, the monthly price gain was driven mainly by oil prices, which expanded 17.0 percent for the month but are still down 20.6 percent from a year ago. Additionally, seven other key materials prices rose on a monthly basis in June.

- Unprocessed energy material prices increased 8.3 percent

- Fabricated Structural Metal Product prices increased 0.7 percent

- Prepared asphalt, roofing and siding product prices 0.6 percent

- Steel mill product prices increased 0.2 percent

- Concrete product prices grew by 0.2 percent

Several key materials prices declined in June including iron and steel, natural gas and nonferrous wire and cable.

Aggregates Material Trends

Industry results in Q2 2016 again showed quarterly increases in pricing and volume compared to the same period in 2015 for cement, crushed stone and sand & gravel. The decline in asphalt prices related primarily to instability in oil prices.

Cement

The estimated portland cement consumption (22.1 million metric tons) increased by 1.3 percent in Q2 2016 compared to Q2 2015.

Ready-Mix Concrete

Ready-mix concrete (RMC) prices continued to rise in Q2 as measured by the average RMC net selling prices of U.S. Concrete, Vulcan Materials, Martin Marietta and Eagle Materials during the quarter. Quarterly RMC volume data is not reported.

Crushed Stone

An estimated 377 million metric tons of crushed stone was produced and shipped for consumption in the U.S. in Q2 2016, an increase of 6.0 percent compared with the same period of 2015. The production of crushed stone increased in six of the nine geographic divisions and 25 of the 44 states that were estimated in Q2.4

Sand and Gravel

The estimated U.S. output of construction sand and gravel produced and shipped for consumption in Q2 2016 was 269 million metric tons, an increase of 6.0 percent compared with the same period of 2015. The production of sand and gravel increased in five of the nine geographic divisions and 23 of the 45 states that were estimated in Q2.4

Headwaters MB is an independent, middle-market investment banking firm providing strategic merger and acquisition, corporate finance, and merchant banking services through proprietary sources of capital. Named “Investment Bank of the Year” by The M&A Atlas Awards in 2015, Headwaters MB is headquartered in Denver, with six regional offices across the United States and partnerships with 18 firms covering 30 countries. For more information, visit www.headwatersmb.com. To discuss any information contained in this report, contact the Headwaters MB team: Darin Good, managing director, [email protected], 303-549-5674; Brian Krehbiel, vice president, [email protected], 303-531-5008.